How Can a Non Resident Indian (NRI) Invest in a Mutual Fund in India?

Shruti Sharma -

Jun 10, 2022

Shruti Sharma -

Jun 10, 2022

Whenever asked about their investments in India, NRIs usually give a list of properties they've bought in the last several years. This needs to be recognized that real estate is an asset class like any other, with advantages and disadvantages. Let's start exploring other options by asking the question, “Can NRIs Invest in Mutual Fund in India?”

In India, NRIs are permitted to invest in mutual fund schemes. Except for NRIs from the United States and Canada, most Mutual Fund Schemes in India are open to NRIs from all over the world. Due to regulatory regulations, there are limitations. They can invest only in the schemes of some of the fund houses such as Birla Sun Life, DHFL Pramerica MF, ICICI Prudential, L&T MF, PPFAS Mutual Fund, SBI, Sundaram, UTI Mutual Fund, TATA Mutual Fund, Reliance Mutual Fund, and Franklin Templeton Mutual Fund. Investocafe not only guides you towards best fund selection but provides best of wealth creation and management services.

How to Invest in India

- Non-Resident Indians can make investments through their Demat account, which is linked to their NRE/NRO account.

- They can also manage their investments through an online platform such as Investocafe

- By granting Power of Attorney (POA) to a family member in India, NRIs can invest in Indian mutual funds.

Advantages of Mutual Funds for NRIs

- Diversified folio with best risk-return trade-off.

- High liquidity to match your cash requirements.

- Managed by professional to give benefit of expert investment decisions

- Any amount can be invested & Investocafe provides a dedicated Relationship Manager to each client.

- Easy to invest and manage digitally; Investocafe investment & wealth management is totally paperless.

- Some mutual funds have tax advantages, if that is the goal.

Details on investment amount and repatriation

Mutual fund investments can only be made in Indian rupees. The money must be taken out of the NRE or NRO account. A Foreign Inward Remittance Certificate is required for any other remittances.

The redemption profits from the sale of MF will be credited to the investor's corresponding NRE/NRO bank account. Only INR will be accepted for redemption. If the investment was made as a Non-Resident Indian and from an NRE account, the redemption proceeds can be entirely transferred back outside on a repatriation basis. Redemption proceeds held in an NRO account are difficult to repatriate.

Requirements for an NRI Mutual Fund Investment

KYC for NRIs

To invest in mutual funds, non-resident Indians must complete a KYC process. Even though they were KYC compliant as resident Indians, they must file for a new KYC. It can be done fully online at Investocafe.

Redemption

Non-Resident Indians (NRIs) must have an NRO or NRE account in order to transfer monies to and from the MF. In India, a bank account opened in another country cannot be utilised to invest in mutual funds.

Other Requirements

FACTA and CRS self-declarations are also required of non-resident Indians. The form is available for download on the AMFI, MF, and KRA websites. The required papers, such as a PAN, passport, and proof of overseas residency, must be supplied. An advisor or the Indian embassy in the country of residence can do an in-person verification, or in many circumstances, this can be done online.

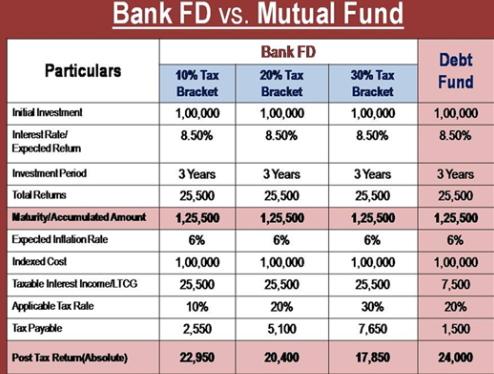

Mutual Fund taxation for NRI

Equity Mutual Funds

Short-Term Gains – 15% of the gains is payable as tax

Long Term Gains – Gains up to Rs. 1,00,000 per year are exempt from tax. 10% tax is payable on gains over and above that amount.

Non-Equity Funds

Short-Term Gains – 30% of the gains is payable as tax

Long Term Gains -If it is a listed MF, 20% of the gains is payable as tax (with indexation). In the case of unlisted MF, 10% of gains are applicable (without indexation)

Fixed Maturity Plans

Tax on Short Term Gains

If the FMP matures in less than 3 years, tax is applicable as per the income tax slab of the individual.

In the case of long term gains, 10% tax, without indexation is applicable and 20% with indexation

Nominees and joint ownership

NRIs can invest in mutual funds in India with another NRI who has completed the KYC process. (his/her bank account information is not required). For mutual fund investments, a non-resident Indian can appoint an NRI or a resident Indian as a nominee.

There are variety of mutual fund schemes. As an NRI, you must choose the appropriate funds to invest in. The fund's performance, your financial situation, financial needs, investment cost, and market conditions all influence your decision.

Start investing Now! Book one free portfolio review with investocafe, if you're confused how to choose the proper investment.

Contact Us @ 7224051610 or write at info@investocafe.com

Know your risk profile at https://investocafe.com/

To get in touch please visit us at investocafe.com

Related Posts

Follow Us

Subscribe to our newsletter

![]() © 2026 All Rights Reserved By Investocafe.com

© 2026 All Rights Reserved By Investocafe.com