Jingle bell Jingle bell, 7th CPC on the way

Anvesh Pandey -

Jul 18, 2018

Anvesh Pandey -

Jul 18, 2018

Its time for govt employees to call out hooray..

Waiting period for Central Government Employees and pensioners is about to come to an end. The implementation of 7th CPC is not so far as state elections are over and results have come. All beneficiaries are eagerly waiting for it to happen and are ready with their shopping list. Since the payout will be lupsum and hike in salary, RBI has already raised eyebrows on the kind of impact it is going to bring on countries balance sheet(estimated around more than Rs 1 lakh Crore), but will also contribute to increase in inflation, due to a buying spree from consumers. .

Whatsoever may be the implications on balance sheet of government, but bonanza for employees of Central Government has been decided and can come any time soon, but what could be the winning ways of deploying the cash from wallet and making best use of it. Following are the suggested actions to be done with the money you receive on implementation of 7th CPC;

1. CUT DEBT

– Don’t shock, yes, the right way of using the fund would beto repay any of your pending loans. Any large amount expected should be first utilized for cutting your liabilities. And for all those who were planning to go for vacation or to buy a car or a costly gadget should give a back seat to their plans and rework towards financial growth.

2. DO A ANALYSIS OF FAMILY FUTURE NEEDS

– Before you blatantly start spending the funds you receive as your arrears, take a paper pen and start writing about the possible future needs which you and your family is going to encounter. It can be education of your kids, their marriage, an emergency fund if someone gets ill in family, and yes to cater the retirement needs. Put a full stop to any other plan if allocation has not been made towards these needs, since financing of such needs could be tough if not planned at the right time. Some may give preference to buy a house rather than giving priority to the options mentioned above, but most of the central government employees reside in government given accommodation and have transferable job, therefore they hardly get a chance to live in a house they buy. The thought process of giving a house on rent for additional income is also a subject of debate. It rarely happens that your house is on rent for all twelve months of a year and maintenance of property is also a additional cost, but yes for all those who are about to retire from services or have already taken care of needs of family should certainly look to buy a house/flat as per their requirement.

3. INSURE YOURSELF

– Take adequate insurance for yourself. Look for a plan which gives you only cover, many insurance companies offer pure term plan with meager premium. Don’t fall prey to ULIP’s, or investment plans along with insurance, since these have always proved to be poor investment avenue as far as returns are concerned. On an average an investor should take insurance to the tune of ten times the annual salary he/she draws.

4. BUY HOUSE/LAND

– After taking care of above needs, if this option lies next in your list, yes you may have been taking a right decision, but this requires lot of due diligence at the end of investor. One more key issue is, investor earn good returns when they buy land instead of flats, if the decision is purely investment. But liquidity could always be an issue with real estate and realization of market prevailing prices may also be a tough task. Moreover, to find a faithful broker who brings deal for you is also a factor in which you need to look in. Not only this, being employee of central government, transfers are something from which you can’t run away, so taking care of property is another issue over which investor should think seriously and then take decision.

5. CHANNELISE SAVINGS FOR LONG TERM INVESTMENT

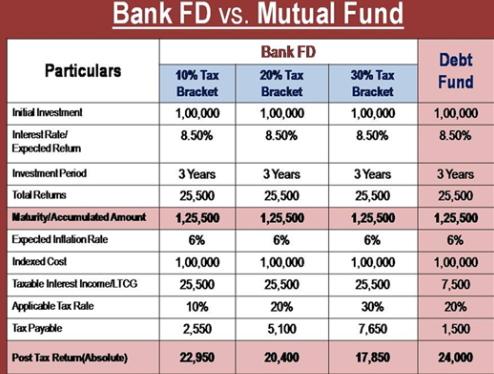

– Another promising investment decision which all central government employees must look into is starting some SIP’s in mutual funds, by taking help of registered investment advisors, they are the perfect instrument for beating inflation and create a good corpus which can actually surprise you if done for ten years or more. Since every employee is getting good 20-25% hike (as expected), must stretch them to invest maximum in the disciplined fashion on monthly basis. SIPs does not put any strain on monthly budget and soon you get accustomed to it. The benefits of such investments are that they are TAX FREE (if investor remain invested for more than a year), and highly liquid in nature.

6. GO ALL OUT

– Still left with cash, now you can go all out and should not stop even if somebody tries to stop you from enjoying, plan for a new vehicle, plan a holiday with family, buy gadgets or any adventure sports which is your dream. This is the time, as you have not only taken care of above stated financial challenges in your life but also catered for any uncertainty or future needs well in advance.

Written By: Anvesh Pandey, SEBI Registered Investment Advisor

To get in touch please visit us at investocafe.com

Related Posts

Follow Us

Subscribe to our newsletter

Tags:

![]() © 2026 All Rights Reserved By Investocafe.com

© 2026 All Rights Reserved By Investocafe.com